Africa’s second largest red metal producer Zambia will be making a fresh appearance in the international capital markets with a re-issuance of fresh bonds following a historic bond restructure consensus reached with Eurobond holders. Tainted the first nation to default in COVID pandemic era, Zambia will be the first nation to restructure debt involving different creditor classes under the G20 Common framework. A quarter of a year ago in November, the red metal producer hit a snag after the International Monetary Fund (IMF) and the Official Creditor Committee (OCC) expressed reservations on an in principle deal the Zambia authorities earlier reached with the bond holder committee on concerns of comparability of treatment. This triggered a rework that has kept the Dr. Situmbeko lead Ministry of Finance on their toes with an earlier forecast to complete the task by 2Q24. The 25 March developments comes as an early Easter gift for the copper producer that currently grapples with El – Niño induced drought impacting power generation and agriculture production set to suffer a 50% haircut in output for the 2023/24 farming season. Zambia debt restructure journey dates far back as November 2020 when the authorities formally applied for financial assistance with the IMF on a journey that only got approval in August of 2022. Last year in June 2023 Zambian authorities, in principal agreed with bilateral creditors on debt treatment for $6.3 billion which was firmed up in October 2023 leaving private restructure as the open obligation for restructure.

READ ALSO: On the Cusp of Debt Restructure, Zambia Restarts Negotiations with Dollar Bondholders

According to Creditor Committee advisors, Newstate Partners and Weil Gotshal & Mangles (London) LLP,” The proposed restructuring terms set out in the 2024 Agreement are based on the same structure as the November 2023 AIP. Two new Eurobonds (further described as Bond A and Bond B in the Government’s press release) will be issued which provide future debt relief commensurate with Zambia’s economic progress in the next few years. While the 2024 Agreement requires both additional debt reduction and net present value relief compared to the restructuring terms agreed pursuant to the November 2023 AIP, it also includes enhanced repayment terms and higher coupons on Bond B, in the event that Zambia’s debt carrying capacity, as assessed by the IMF and World Bank’s Composite Indicator, moves to medium from weak or Zambia continues to meet or exceeds current IMF projections as measured by exports of goods, services and fiscal revenues measured in US Dollars. The 2024 Agreement also includes agreement on certain non-financial terms, including a most favored creditor clause that will ensure that certain other creditors do not receive a better recovery in the restructuring on net present value terms, a loss reinstatement clause if Zambia were to default during the term of the IMF program, and certain ongoing information covenants for Zambia.”

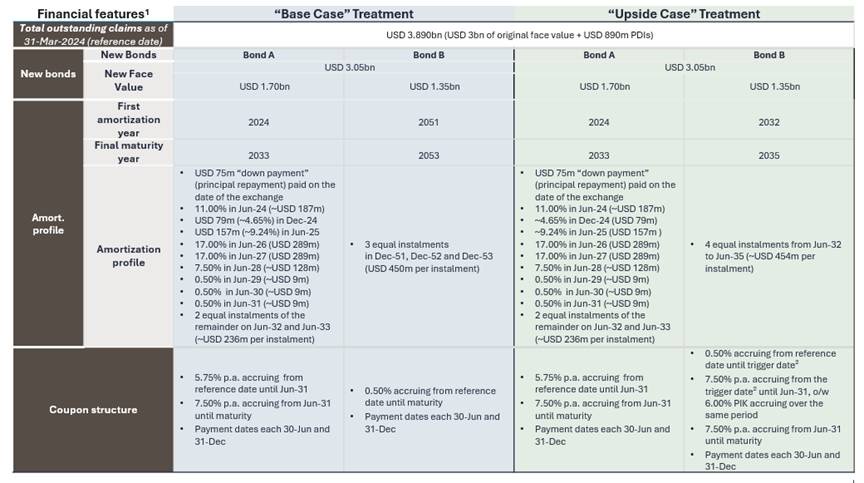

Zambia’s restructured bonds total $3 billion in $750 million (2022), $1 billion (2024) and $1.25 billion (2027) which will roll in two assets for maturity 2033 ($1.7 billion) and 2053 ($1.35 billion) under economic base case scenario with first armotization year in 2024 and 2051 for the two respective bonds.

The restructure agreement also offers an upside case scenario that could seen the $1.35 billion bond mature earlier by 2035 with first amortization year being by 2032.

PROSPECTS FOR ZAMBIA AHEAD

The dollar bond ‘in principle agreement’ if nodded by bond holders will provide relief of circa $3.3 billion as per MinFin statement on its website.

“Today’s agreement with the Steering Committee brings us closer to the completion of Zambia’s debt restructuring, edging us nearer to unlocking substantial resources vital for our developmental aspirations. The agreement to restructure the Eurobonds provides essential debt relief provided by the Bondholders, including foregoing around $840 million in claims and offering approximately US$2.5 billion in cash flow relief through reduced debt servicing payments during the IMF Programme period,” Zambia MinFin carried on its website.

Zambia’s default status was triggered on November 2020 when the copper producer skipped coupon payments on its dollar bonds which has for the last couple of year made the copper producer bear the brunt of unfair capital pricing on account of wide sovereign premiums. This credit assessment downgrade impacted the banking sector that took a negative cue through higher international financial reporting standard (IFRS) credit provisioning, costly dollar credit lines and low credit appetite for sovereign related counterparties. The development puts Zambia on the verge of a credit rating upgrade on its long term issuer rating on foreign currency that kept transfer and convertibility risk elevated. With the strides Zambia has made over the last few years the red metal producer has earned local currency rating upgrades with Moody’s and Fitch to ‘Ca’ and ‘CCC+’ while citing cash flow weaknesses from its frail fiscal position.

READ ALSO: El – Nino effects Forces Zambia into Declaring Drought Disaster, Credit Risks Could Exacerbate

President Hakainde Hichilema’s government will seek to effect aggressive growth over the coming years to absorb the obligations that fall due after over 20 months of non-service of commercial debt. Hichilema also faces a drought quagmire that he has seen as an opportunity to turn Zambia’s agribusiness and power generation prospects higher for the better through temporal extermination of duty and tax on irrigation and renewable energy equipment.

The development shines a light on Zambia and is attracting global interest in its local currency bonds that currently are yielding between 22% – 26% that in turn will provide support to the foreign currency supply bottleneck the copper producer faces. This behavioral pattern is expected when the yield curve is forecast to compress. Additionally expected is a dump of dollars on the market that will give the Kwacha a positive cue but in the short term. The red metal producer has seen some decent flows from mining deals actualizing such as the Mopani transaction and other Chinese related mines, however the debt completion is expected to pave way for more market certainty to attract capital that may have been on the fence for a long time.

With time Zambia’s bonds could bounce back on the JP Morgan Emerging Market Index, a status that was lost after sliding into junk a few months before default as fiscal posture deteriorated.

The red metal producer currently looks to its reorganization of its mining portfolio to support stronger growth especially in the green metals race that is attracting both the west and the east. This has kept copper prices fairly healthy on the London Metal Exchange a positive for Zambia’s cash flow position to cushion debt service. Zambia is also 20 months into a 38 month IMF extended credit facility that continues to make the Southern African nation a darling to the international community.

The Kwacha Arbitrageur