The bourse in Africa’s second-largest copper producer Zambia, the Lusaka Securities Exchange (LuSE) has outperformed the continent’s stock markets with its share index flirting with a fresh all-time high on August 24 to 7,010.4. Trading 15.7% (YTD) firmer in, local currency terms, the index is in dollar terms 19.3% stronger, surpassing the S&P500 index and previous scoreboard winner, the Nigerian Stock Exchange (NSE) currently at 16.3% (YTD). Stock market outperformance for the red metal producer is a barometric indication of its growth and economic recovery prospects underpinning faculties such as mining, banking, energy, manufacturing and agribusiness. This is to a large extent fueled by a plethora of factors including a better sovereign risk outlook, dislocated global grain and food market opportunities, volatile energy markets, decarbonization propelled mining boom and above all post-pandemic recovery.

Despite global risks, the LuSE reflects a broad rally signalling a homogenous economic outlook across the sectors as the economy shrugs off pandemic distress, leverages off silver linings in turbulence and taps into the rising risk appetite seeping into the markets. Of the 23 listed names, 67% have posted gains while 14% shaved value with the remainder unchanged in market capitalization.

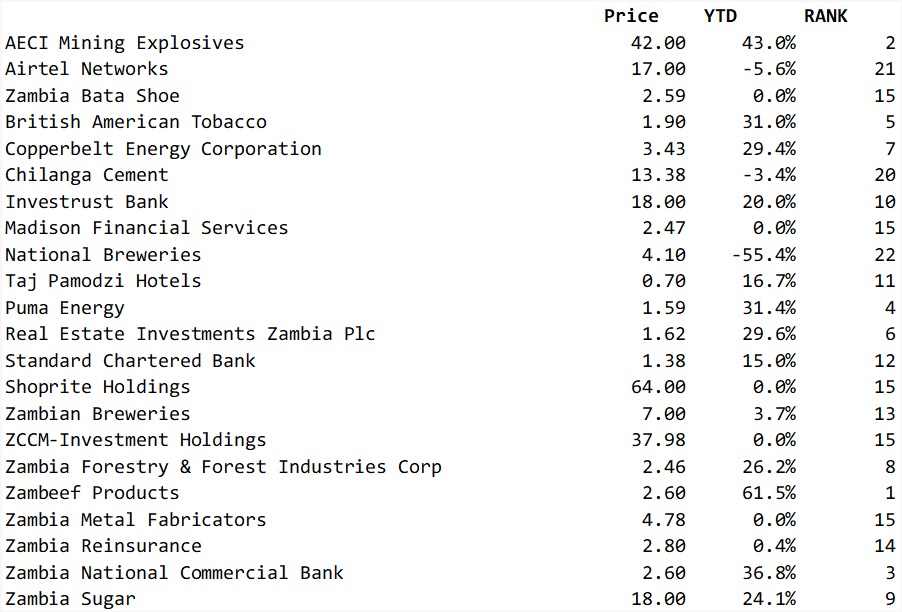

Winning ISINs – Zambeef, Afri-Explosives, PUMA and Zanaco

Drivers of the winning stock market trajectory include Zambeef (ISIN:ZM0000000201) whose share price has rallied 61.5% to K2.6 supported by efforts to double the output of its Mpongwe asset leveraging off scaled wheat prices which the agribusiness entity wishes to plug the regional deficit in chaotic times. Zambeef inked a financing deal with the international finance corporation (IFC) for the Kwacha equivalent of $35 million and remains in the market for $65 million for its expansion program.

African Explosives (ISIN: ZM0000000284) is up 43% this year to K42 a share and continues to take a cue from improved mining prospects after Zambia launched an aggressive reorganization campaign of its mining assets. With greater interest in mining spurred by a stronger global decarbonization drive, interest in battery metals continues to scale demand for explosives whose outlook remains bright with the higher set targets for copper production in a decade to 3 million metric tons.

Zanaco (ISIN: ZM0000000250) has continued on a stellar performance, breaking the barriers in an FY21 K1billion after-tax profit-making its shareholders looking forward to attending the last annual general meeting for value dividends. The big strong reliable bank defied odds to show that an indigenous bank being the largest by asset size could also outperform international peers. Market expectations remain sanguinely high, making this banking stock the most attractive to buy in its faculty. Zanaco’s 1H22 profitability remains ahead of the curve and is priced into shareholders’ appetite for the stock with an outlook of an even better FY22. The big strong reliable stock has rallied 36.9% year to date to K2.6 per share representing the third largest appreciation on the score board. This winning streak is forecast to extend into 2H22.

In the faculty of petroleum PUMA energy (ISIN: ZM0000000194) continues to take a cue from elevated crude prices in the wake of supply constraints orchestrated by the Russo – Ukrainian war. The volatility of the petroleum market for Zambia with the energy regulator reviewing prices monthly has seen more hikes than ebbs. This has given oil marketing companies (OMCs) more positive cues on margin. However, on the downside in the long term, the global ESG agenda could threaten the existence of fossil fuels that could dent performance. PUMA stocks are 31.4% higher on a year-to-date basis trading for K1.59 a share.

British American Tobacco (ISIN: ZM0000000029) typical of a sin stock is rallying with post-pandemic recovery. BAT stock has rallied 31% to K1.9 a share on higher sales roughly 23% in 1H22 with a more cost-efficient model. Smuggling risks were exterminated given a weaker Kwacha at the start of the year and could likely resurface with Kwacha appreciation.

The cigarette retailer successfully localized its debt which has helped keep margins healthy.

Losing ISIN’s– Natbrew, Airtel and Lafarge

National Breweries (ISIN: ZM0000000086) leads the curve of stocks on a losing streak with a 55.4% decline in price year to date to K4.1 per share. The opaque beer producer grapples with illicit beer manufacturers pushing production costs wider and sales lower.

Despite strong profitability, Airtel’s (ISIN: ZM0000000342) share price ebbed 5.6% to K17. The telecom giant is faced with fading voice calls as markets embrace data means with the emergence of MiFi devices by internet service providers (ISPs). Unique about Airtel is that shareholders still do not partake in the spoils of Airtel money which is a separate legal entity and is not part of the listed vehicle. The mobile network operator has positive cash but with a fairly high debt to current asset ratio signalling elevated gearing.

Lafarge Zambia (ISIN: ZM0000000011) ebbed 3.4% to K13.38 seemingly overpriced after the takeover by Huaxin which owns a 75% stake. The cement producer faces hurdles in the area of export with currency strengthening which leans the entity’s margins. Other threats the entity faces include a slow down on government infrastructure spending. However, on the positive Lafarge has a strong cash position and is in debt free a position earned as a result of the changes at the shareholder level as Huaxin controls a 75% stake.

The Kwacha Arbitrageur