According to a note by BMI Fitch Research, Zambia will struggle to achieve meaningful fiscal consolidation. The research firm believes that Zambia’s government will struggle to enact rapid fiscal consolidation over 2019 and 2020, as the government will keep public spending elevated despite calling for fiscal consolidation in the budget speech released at the end of September. BMI is of the view that revenue-enhancing tax reforms – which will be implemented by January 2019 – will hit mining production and private consumption in an already weak economic environment, meaning that receipts are unlikely to reach government targets.

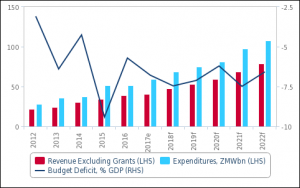

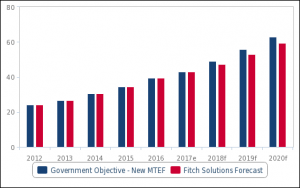

BMI projects higher fiscal deficits than forecasted. While we forecast the fiscal deficit to reduce from an estimated 7.5% of GDP in 2018 to 7.1% of GDP in 2019, we forecast it will average 6.9% GDP over the next five years, well above the 3.9% GDP average registered over the past decade and above the predictions made by the government in its Medium Term Expenditure Framework for 2019-2021 (5.6% of GDP), BMI said.

Rising borrowing costs and the absence of significant expenditure reductions will mean that Zambia’s external debt will continue to increase over the next two years, posing severe risks to growth in the country.

Expenditures Continue To Increase, Despite Calls For Consolidation

Zambia – Budget Deficit (% GDP), Revenues & Expenditures (ZMWbn)

An analysis of the 2019 Budget speech suggests that the government will struggle to meaningfully pare back spending in the short term. It is expected that rising yields on the 2024’s (dollar bond) to trigger a shift to stronger fiscal austerity, expenditure plans outlined by the Finance Ministry at the end of September will fail to significantly reduce Zambia’s fiscal deficit in the short term. While the 2019 budget called for ‘increased fiscal consolidation’, planned expenditures are slated to increase to 28.2% of GDP from 25.9% GDP in 2018, with a significant ramp-up in capital expenditures.

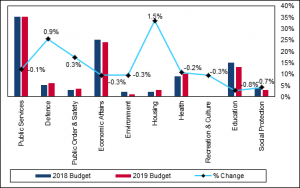

Zambia’s large infrastructure gaps – especially in transport and energy generation –remain a major issue for the country’s long-term growth, and the government increased allocations to infrastructural projects in the 2019 Budget by 18.1% to about K12.5bn (or 14.0% of total expenditures). The planned expenditures will be directed especially towards road and energy infrastructure, financing the Link Zambia 8000km project, Copperbelt and Ndola International Airports – for which budget allocation increased by 70.2% – and 1200Mw Luapula Hydropower project. That said, project execution rates in the country have been poor. Indeed, the World Bank recently estimated that the cost for building one km of road in Zambia amounts to USD350,000 in 2017, almost double the average for Sub-Saharan Africa. We thus expect these infrastructure projects to fail to break even or generate returns in the short-to-medium term, leading to an increase in debt. Moreover, as the majority of these projects are only around 13.0% complete, increased contraction of project financing will contradict the austerity measures proposed by the government in June, which restricted fiscal support to projects close to an 80.0% completion rate (see ‘Zambia’s Fiscal Consolidation To Bring Only Temporary Relief’, June 19). We believe this is set to increase investors’ concerns over the government’s ability to adhere to its fiscal commitments, sending yields on Zambia’s debt higher.

Spending Allocation Will Remain Inefficient

Zambia – Proposed Spending Function As % Of Total Budget

Moreover, several structural rigidities will temper the pace of fiscal consolidation in the medium term. Firstly, a substantial portion of the budget over the next two years will need to be focused on paying off the arrears accrued during 2015 and 2016. Indeed, arrears to private sector creditors increased by 571.5% in 2016 as the government kept financing several development projects while maintaining high levels of current expenditure to support farmers during the 2015-16 droughts, as well as financing the political campaign during the 2016 election. Secondly, the rising cost of interest expenses will represent an increasing burden for the government, draining resources meant to fund other expenditures. Interest payments due on Zambia’s debt will increase from 29.0% of total revenues in the 2018 budget to 42.0% in 2019, and we think they will remain elevated in the coming years, as the government plans to take on additional external debt – expecting external financing to represent 85.0% of total infrastructure project financing in 2019. Indeed, the administration’s new Medium Term Expenditure Framework (MTEF) released in September expects interest payments over 2019-2021 to average 22.5% of total revenues – an increase from the 19.5% average calculated in the previous MTEF released in August 2017.

Finally, absence of the approval of key structural expenditure management reforms will make the implementation of any austerity plan challenging in the years ahead. Indeed, Zambia’s high decentralisation of the public investment management system – which gives local representatives a significant degree of independence in raising capital to plan and implement their own investments – will continue to weigh on fiscal consolidation in the absence of significant reforms. The Public Procurement Act and the Loans and Guarantees Act CAP 366, proposed by the government at the start of 2017, would increase parliamentary oversight of the debt contraction process by local representatives, and could thus strengthen efficiency in expenditure management. However, the government remains deeply divided on parliamentary oversight, and we don’t believe that these measures will be passed in the short term. Moreover, we believe that the government is unlikely to obtain the USD1.3bn IMF loan that would have served as a critical policy anchor for the swift approval of these acts

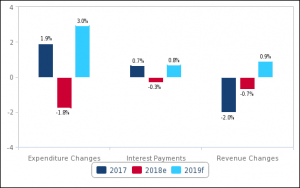

Consolidation To Remain Slow

Zambia – Fiscal Consolidation Measures

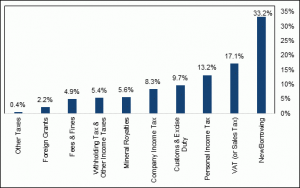

While the government plans to enact the bulk of fiscal consolidation by increasing revenues, we expect that proposed measures will hamper growth in the economy, leaving debt financing at the core of the fiscal strategy. We believe that a series of tax increases on mining companies operating in Zambia will weigh on output and production in the sector, presenting serious headwinds to growth in the economy. Indeed, despite a positive outlook for copper prices in 2019 – copper accounted for around 70.0% of the country’s exports over the past decade – our Mining team has significantly revised down its forecasts for 2019 production from an expected 6.0% and 8.0% in 2019 and 2020 to 5.0% and 4.0%, respectively. As mining and mineral royalties accounted for 4.2% and 43.0% of tax and non-tax revenues, we believe that a decrease in mining activity due to increased business operation costs will constrain revenue growth, meaning that the government underperforming revenue targets over 2019 and 2020.

Government Revenue Projections Remain Too Bullish

Zambia – Revenues Projections, ZMWbn

This will increase debt in the short-term, raising macroeconomic risks in the years ahead. To maintain the elevated level of expenditures planned in the 2019 budget, the government will need to increase external borrowing in the coming years, which will weigh on Zambia’s macroeconomic stability. Investors’ concerns over the government’s ability to repay its debt obligations has already triggered a sharp sell-off in the Zambian kwacha, depreciating the unit by 20.0% in the month of September. The government’s expansionary plans are unlikely to improve investors’ sentiment, pushing the kwacha’s value even lower, which will see inflation increase over the coming months. Coupled with weak credit growth caused by high levels of government domestic debt – which are already generating significant crowding out effects – the sell-off will weigh on consumption and non-mining sector activity, underscoring our forecasts for GDP growth of 3.0% in 2019 and 3.8% in 2020 – well below the 6.3% average for the past decade.

Debt To Continue Increasing Over 2019

Zambia – 2019 Budget Financing, % Of Total Expenditures