The central bank in Africa’s second largest copper hotspot, Zambia will today commence deliberations on monetary policy for the next three months. This rate decision meeting will run for two days consecutively to announcement on Wednesday 17. Bank of Zambia Christopher Mvunga is in the face of a an overvalued currency, the Kwacha, and a spiraling inflation labyrinth all happening on a COVID clock which is believed to dis-incentivise the monetary policy committee from adjusting rates any higher despite fundamentals signaling the need to hike. Zambia’s benchmark interest rate (BPR) has been kept tad at 8.0%, for the last 6months, the lowest the copper producer has experienced since it started tracking the monetary policy rate.

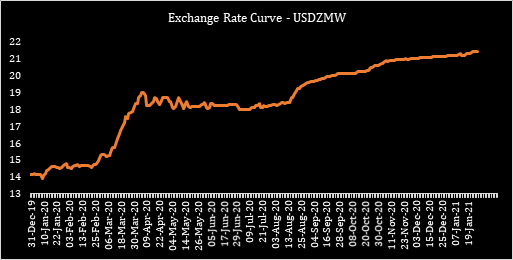

With a confluence of economic woes fueled by rising external debt burden, the Kwacha has extended its losing streak this year shaving 1.31% as it trades north of 21.5 for a unit of dollar, while inflation spiraled 230 basis points to a 57month high of 21.5% in January sending treasury bill yields (save the 1yr), under- water. Underwater is a terminology used to depict yields that are below inflation whose tenors make it unattractive for locking in liquidity for investment. The last monetary policy committee meeting, Mvunga’s debut, kept rates unchanged at 8.0%, however economic fundamentals have continued in fragile zone with Kwacha weakness playing a pivotal role in breeding cost push inflationary pressure both for inputs (for manufacturing purposes) and consumer related prices.

COVID19 ADJUSTED THEME IN RATE DECISION MEETING (MPC)

It is about a dry point of construction that the COVID year 2020 had exceptional decisions in the monetary policy space which saw rates eased to lows to help cushion credit repayment burden of consumers and record liquidity injections and quantitative easing techniques through open market operations (OMO) backed by an aggressive bond buy-back program, swapping short dated for longer dated fixed income paper. This was homogenous across global central banks which the Bank of Zambia were not exempt.

Overlapping events can not be overlooked as drivers of sentiment in the market such as the two defaults that Zambia suffered being the $42.5million on November 13, last year and the $56.1million on January 29, of this year. This would have in essence brewed asset sell off pressure or dollar capital flight but for the natural hedge posed by the widening backlog which have eased pressure temporarily. Credit default spreads remains wide as credit risks remain elevated. Non performing loan ratio domestic credit remains above the 10.0% prudential threshold at 11.6% while transfer and convertibility (T&C) risks remain high on the back of currency depreciation.

SPIRALING INFLATION VS NEED TO EASE CREDIT RISKS – QUAGMIRE

Ideally, inflation bears sending the yield curve, on the short end, 150-750bps underwater signals an aggressive uptick in rates as the term structure of interest rates gears to correct. Currency depreciation in Africa has been effectively managed through tightening liquidity through raising statutory reserves or hiking the benchmark interest rate. However in disease pandemic times, central bank decisions are becoming more and more adjusted for social concerns as the monetary side has a task to balance between financial sector and price stability versus effectively managing disease pandemic induced credit risks.

Zambia’s rising cases and likely impact on the business ecosystem will be the biggest determinant in the monetary policy committee stance. Additionally, the market is eager to be guided on what measures the central bank will institute to manage the widening backlog and address the overvalued Kwacha. Interim measures to shore foreign exchange reserves using gold purchases through the actualization of the Gold Purchase Agreement (GPA) are more long term to supplement the mining tax receipts in dollars directly to the central bank which is clearly inadequate.

It is very unlikely that the Mvunga chaired MPC will lower rates any further, neither will they be incentivized to hike rates as doing so would hurt the credit environment in disease pandemic times. However some actions in the currency faculty will be very crucial in taming spiraling inflation and will simultaneosly cure ailing business pulse. An 85% probability for a no rate change is attached while 15% likelihood will be reserved for an infinitesimal hike to curb Kwacha depreciation.

The Kwacha Arbitrageur