Africa’s second largest copper hotspot Zambia is grappling with a foreign exchange quagmire whose symptoms manifest in persistent depreciation. The paradox surrounding whether a weak or firmer currency is preferable rests with which side of economic activity players are positioned, supply or demand.

The copper currency, the Kwacha has been on a losing streak against what most had expected especially after a $6.3-billion bilateral debt treatment was sealed in June on the sidelines of the Emmanuel Macron led Global Finance Summit. Let alone when the International Monetary Fund board approved disbursement of the $188-million second tranche of the $1.3-billion extended credit facility pressure has not significantly eased.

Amidst earlier market weariness following delayed approval of the second ECF tranche when the IMF Mission team reviewed Zambia in April, Zambia had already started experiencing headwinds in the mining sector given environmental factors in excess rain in the Copperbelt of Africa adding more production pressure to the current Konkola and Mopani Copper Mines muted operations that has cost the Southern African nation its traditional copper target. The red metal producer is forecast to record 10% lower output in 2023 which will be a 14 – year record low of 682,675 metric tons.

This dutch disease syndrome has cost Zambia a downgrade in growth this year to 2.7%, accounting for 200-basis points lower than previous year. Lower copper production does significantly shock foreign exchange markets as such weighs public finance cashflows and general dollar supply.

In its third rate decision communique for the year, the Bank of Zambia intervened 22% lower in the foreign exchange markets with $300-million on account of 51% contraction in mining flows in the first half of the year. Dollar reserves ebbed $200-million to $2.7-billion accounting for 2.9-months of import cover in 2Q23 declining from 3.3-months of cover in 1Q23.

AGRIBUSINESS & NET USD PAYING POSITION WEIGH

Zambia’s net dollar paying position does not support a stronger currency as such continues to widen demand for forex because growth for the Southern African nation entails importation of equipment, goods and services. This has been the case due to the weak manufacturing posture of Zambia with not much it produces for the export market to significantly earn the economy dollars on the supply that would counter rising demand for import purposes.

Although the land linked nation being a net exporter, since a large portion of those are not housed domestically, Zambia is a net payer of foreign exchange.

Central Bank Governor Dr. Denny Kalyalya in his Monetary Policy Committee presentation attributed the widening to $198.1 million (3.1% of gross domestic product) from $188.7 million in 1Q23 to due to higher import velocity from economic actors. This is forecast to balloon to under a billion this year spelling further currency bears.

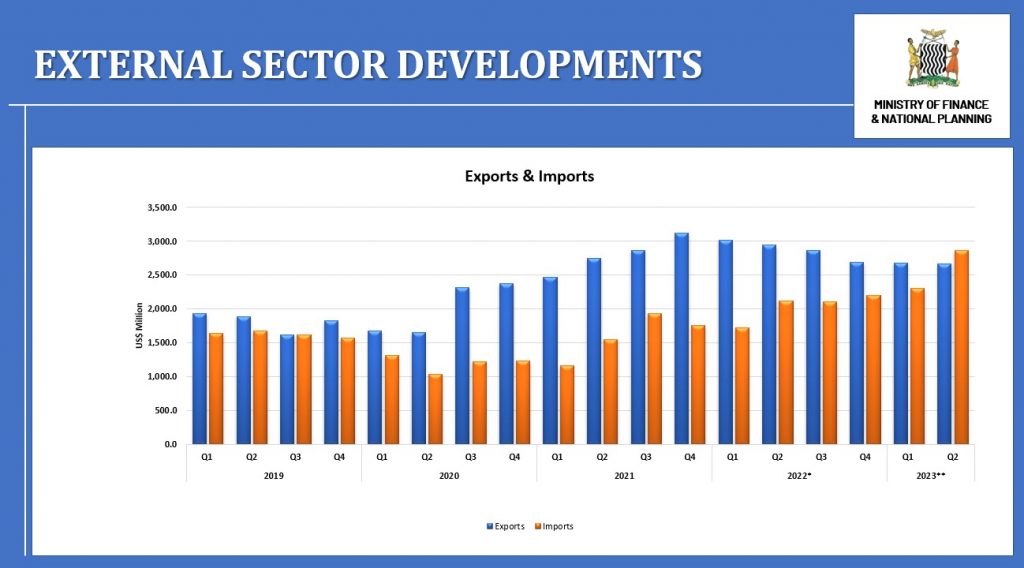

In a telephone interview Executive Head Trader for Opportunik Global Fund Dean Onyambu said, “Over the last 5 years, Zambia has predominantly delivered a current account surplus. That said, we have now seen 3 consecutive quarters of current account deficits from 4Q22 – 2Q23 largely on the back of copper production challenges, as well as rising imports. In this period exports have stagnated at around $2.7 billion per quarter, down from $2.9 billion on average, in the preceding 3 quarters. Meanwhile, imports were higher to around $2.9 billion in 2Q23 from $2.2 billion in 4Q22.”

Going forward, a quicker resolution to the Mopani and Konkola Copper Mines is needed to address the overall trajectory of red metal production from existing mines. Furthermore, September has traditionally been a poor month for the Kwacha. That, in conjunction with declining foreign exchange reserves, a protracted resolution to the debt restructuring saga, impeded copper production, underscores that there could be significant pressure on the Kwacha over the next few months, Onyambu advised.

As the agriculture season looms, another driver of foreign exchange pressure is input supply that does exacerbate dollar demand to fund fertilizer imports. Zambia is yet to address its farming input manufacturing capability which it has struggled with since the state owned Nitrogen Chemicals of Zambia was faced with operational hurdles on account of obsolete equipment requiring capital injection for state of the art technology. As part of the farmer input supply program the agriculture authorities have resorted to sourcing fertilizer from neighboring nations whose prices still price in geopolitically induced high crude and potash costs (input inflation) keeping the purchase costs elevated. Some investments have been recorded in the manufacturing sector such as United Capital and Africa Fertilizer but yet to expand to absorb the national demand significantly to flatten foreign exchange pressure. Until more players influx in the fertilizer market, the cyclical agribusiness dollar pressure will persist in the fourth quarter of each year.

Commenting on the matter First National Bank Economist Chileshe Moono said, “The current depreciatory trend is mainly a function of the mismatch between demand and supply levels on the domestic market. In the coming months, we expect this mismatch to widen as demand from the agriculture sector lifts in preparation for the summer planting season.”

On the supply side, we could see some reprieve on the back of improved production levels from the mines – which will enable the central bank to supply more USD to the market. The successful completion of the 2nd IMF review in October could also provide support in the form of actual hard currency and a new wave of sentiment support for the Kwacha. That said, we still expect the increase in demand to outstrip the support. A break of K20.00 psychological levels is probable in the coming weeks, Moono told the Telegraph.

PROLONGED PRIVATE DEBT RESTRUCTURE

The copper producers sovereign outlook has improved following the debt restructure agreed with bilateral creditors to the tune of $6.3 billion however it remains critical that the private credit is fully addressed before Zambia can have it foreign currency long term issuer rating improved from current default status by international rating agencies. Signs of positivity can be depicted from the recent Moody’s upgrade from Caa3 from Ca on its local currency issuer rating taking into account the strides the Southern African nation has taken this far. Debt reorganization complexity nonetheless remains another source of uncertainty as markets relentlessly seek clues surrounding progress. One thing that remains clear, is that only when memoranda of understanding are signed will tangible assurance be given to private creditors. It remains unclear how long this process could take and for investors, this could be a risk factor impacting investment decisions.

The market has in the last two bond sales (July and August) seen increased interest in Kwacha sovereign paper on longer dated tenors between 7-10 years as offshores bullish on Zambia take long views on the copper producers recovery prospects. However it is very evident that the Southern African nation requires urgent intervention to address structural issues from fiscal restoration to mining incentives if it is benefit from the higher copper prices on the London Metal Exchange whose wave provides an opportunity for commodity exporters to balance their current deficits.

Hakainde Hichilema, Republican President and Zambia’s Chief Marketing & Investment Officer continues to seek opportunities to spur the influx of foreign direct investment and has maximized usage of economic policy diplomacy with the most recent being attendance of the BRICS summit in Johannesburg, South Africa. Most investors have kept their eye on Zambia in 2023 especially that the budget cycle draws nigh with key expectations surrounding the sectors such as mining and also that this is the first budget after the bilateral debt treatment which does spell significant savings over a 10 year period which is expected to shift the copper producers production possibility frontier.

The Kwacha Arbitrageur