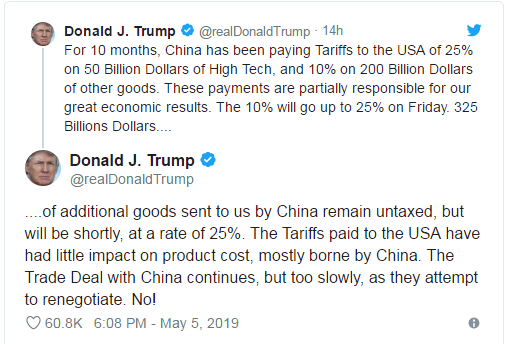

With moods on the fence as investors remain optimistic about the new clues about market direction in Q2, Donald Trump dampened the mood when he just threatened to slap 25% of tariffs on $200 billion worth of Chinese goods on a Sunday 05 May. Trump believes the trade impasse talks are moving at a snails pace and needed some jump starting. However this has made China think twice about continuing talks this week.

Vice Premier Liu He was to leave on 08 May for Washington but this might not happen until the major powers resolve this deadlock.

Asian shares are bruising 6% as Wall Street nursed 2% in early trading. Crude markets are 2.3% weaker as WTI US futures are trading for $60.89/bbl with the ICE Brent shaving 75 cents to $69.89/bbl. Other factors weighing crude are rising inventories in the United States and forecasts that OPEC nations will increase production to plug the gap created by the sanction waiver lifting for the 8 nations that previously bought Tehran oil.

Most currencies are at lows with the offshore Yuan at 6.845 levels close to Jan trough, the Euro was weaker at 1.1186 as the DXY held unchanged at 97.538 making spot gold jump 0.34% to $1,282/ounce.

COMMENTARY

Its going to be a very tense week that could potentially unwind all progress made on the trade talks in the last few months. Global markets have suffered asset valuation over the US – China trade impasse and this just adds a new adverse dimension to sentiment in light of growth and global aggregate demand. Already the manufacturing pulses are gloomy for Europe, China and the United States, additional pressure will only make appetite for riskier assets worse.