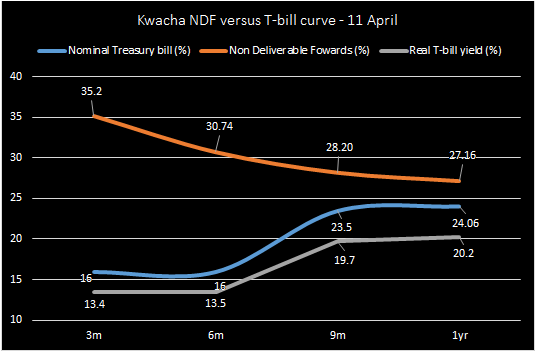

The Kwacha Non Deliverable Forward (NDF) Curve is at spreads of between 310 to 1,920bps above the nominal treasury bill curve as at last Thursday 11 April suggesting that government securities could be slightly overpriced. Ideally the NDF curve should be at most, close to par (in developed markets) or at negative spreads on the T-bill curve (usually in frontier markets). Spreads between Kwacha NDF and T-bill market have turned positive (are widening significantly).

See below the Kwacha offshore non deliverable forward rates versus the nominal and real treasury bill curve as at 11 April.

The current fundamentals reveal that the treasury bill curve is underwater by significant spreads. An example is the 1-year T-bill which is at a 390bps discount to the one year NDF point while the widest discount is in the 3-month bucket is paying 16%, a 1,920bps below the NDF yield.

What rising NDF yields could be signaling?

NDF curves are of offshore nature reflecting perceived sovereign (as measured by Fitch/Moody’s/S&P ratings) and convertibility risks as they do price – in perception from economic sensitive data. Treasury assets such as bills and bonds on the other hand should reflect liquidity, currency and sovereign risks to the extent that, if markets were perfect enough, the underlying reference rate would be the base for NDF’s. Suffice to say the Kwacha NDF curve would be a subset of the short term govie curve. However what obtains in reality is that NDF rates are now blowing out to levels higher than government securities which is an anomaly and signalling sentiment risk by offshore potentially due to asymmetries in information. (Offshore’s give a picture of what a liquidity market would respond like compare to domestic markets which may be managed by central banks in their mandates to carry out monetary policy aligned to economic growth)

NDF’s at a premium to treasury bill yields could signal souring sentiment and a such a higher credit risk premium required to compensate offshore players for perceived sovereign risk. This is exactly what the capital asset pricing model tries to explain. It could also be a reflection of an under- priced or managed government curve. This poses a challenge as it makes assets unattractive eventually. A widening gap also reflects the nervousness of investors in the offshore market if we analyse it from a confidence perspective because the NDF curve can proxy sentiment.

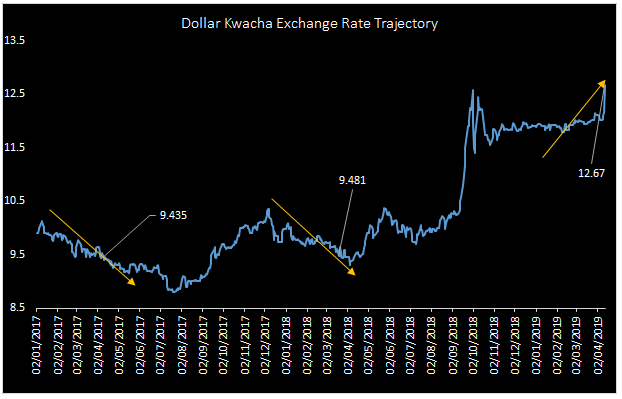

The NDF spreads started to widen after news around low reserves, import cover and debt concerns were more pronounced last year. Wider gaps have been observed recently after the trajectory was persistently declining. This has heightened currency risks as seen by a depreciating Kwacha against the dollar which is seen as bearing the brunt of the fiscals. However, the positive out of this is that allowing a currency to reflect the macro’s, hedges the economy from recession risk. This can be argued by economists that this paradox only holds in bigger well diversified economies. to some degree we believe its holds for all frontier markets.

Nations like Nigeria and Angola that have a record for managing their floats have ended up in recessions while the likes of Zambia and Mozambique despite economic challenges have only been exposed to slower than usual growth by higher every year than previous.

Other proxies for offshore sentiment are credit default spreads (CDS’s) which widened an average of 338bps in the March period and are currently at 1,312bps (2022), 1,336bps (2024) and 1,194bps (2027) above similar tenured US treasuries.