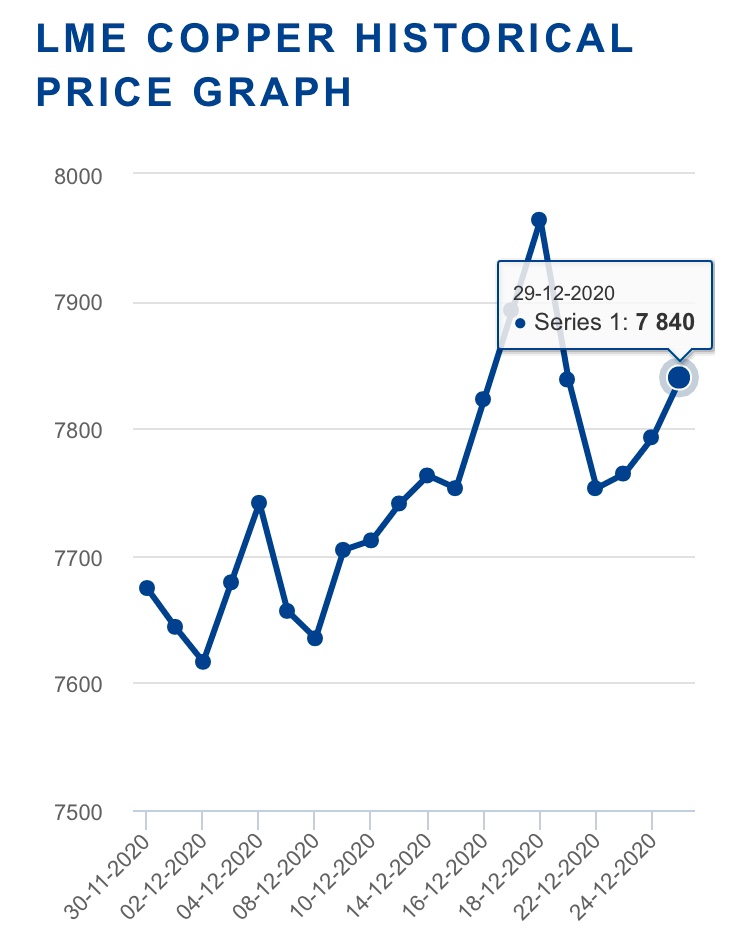

With copper rallying over 76% (from March lows of $4,343 a metric ton) when supply chains bore the brunt of disease pandemic globally, to flirting with highs of $8,000 a metric ton, levels not seen in 8years on the London Metal Exchange (LME), Zambia’s mining prospects are begining to brighten. This outlook is double pronged stemming from new mines in the new Copperbelt of Africa dubbed Zambia’s North Western province and the opportunities that exist through restructure of existing mining assets on the Copperbelt Province of the Southern African nation. See below the copper price graph per metric ton.

_________________________________________________________________________

Mining production was last September reported at 9.5% higher than a year ago at 646,111 metric tons up from 590,321 metric tons by the mines ministry. Copper is to Zambia what crude is to the Middle East such that a rally in prices bellwethers improved outlook and a stabler exchange rate seeing that the sector accounts for over 75% of the Southern Africa’s foreign exchange revenues.

Read also: LME Copper hits 8yr high, the new ‘Copperbelt of Africa’ to drive Zambia’s economic recovery

Despite the price boom as world economies reopened, Zambia’s mining sector remains gutted by a confluence of risk factors that include litigation proceedings, care and maintenance business review decisions , energy supply stability concerns and double taxation as non tax deductibility of mineral royalties remains a key pain point weighing exploration investment appetite. These items of issue do potentially weigh on mining investment propensity fueling Zambia’s production capacity inertia, capping it at a few thousands of tons to below a the million benchmark, tagging behind the Democratic Republic of Congo – DRC.

Read also: As copper flirts with new highs of $8,000/MT, Zambia looks to mining to expedite economic recovery

KONKOLA MINES EARMARKED FOR RESTRUCTURE & REORGANISATION

According to a management brief circulated to Konkola Copper Mines staff on December 28, a decision on mine restructure had been reached by management, in the quest to restore the technical health of the mine. The mining entity will be reorganized into two separate subsidiary companies, namely KCM SmelterCo Limited, and Konkola Mineral Resources Limited, in a bid to increase efficiency and business opportunities, as well as foster optimization. KCM SmelterCo Limited has been in existence since 2002 and has been a fully- owned KCM company, save it has been a dormant subsidiary.

With an ongoing arbitration process, it may on the face of it seem confusing because a restructure or reorganization decision would ideally be arrived at after consensus at board level with shareholders consent. How then was this achieved given that an arbitration process is ongoing? The management brief, tells staff that the Provisional Liquidator, Mr. Milingo Lungu, and the Company Management have been working towards restoration of the technical health of KCM, which commenced with the Winding up Petition by ZCCM-IH in the Lusaka High Court on May 21, 2019. This reveals that the mine is still under care of the liquidator with an acting Chief Executive Officer (CEO) which conflicts with what would ideally be expected under arbitration with both parties on opposite ends namely ZCCM-IH Plc and Vedanta Resources the majority shareholder still in talks following a litigation seesaw experience. The last higher court ruling, the court of appeal, stayed the ongoing liquidation proceedings and rather guided towards arbitration.

KCM remains a very strategic and emotional asset for Zambia with copper ore grades ranging between 2.5% to 5.5%. The restructure echoes an array of opportunities for Zambia key of which includes ring fencing the mines earning capacity and will help realize the assets benefits in a fashion that will make it attractive for equity investors. The restructure exposes the smelter potential and the mining license which could allow investors that would be interested in copper and cobalt mining while the Zambian authorities navigate ways of structuring shareholder agreements in a way that does not disadvantage citizenry for mineral resources mined in their backyards. Further it is highly unlikely that the next owner of the mine, should Vedanta lose this battle, would be interested in the exact shaft sank where the current majority shareholder drilled it, but will look to maximize other expanse areas that the license caters for including cobalt reserves. An injection of $1.5billion will nonetheless be required to make the mine functional. And with greenfield projects on the horizon such as electric car era and lithium battery driven cobalt boom, Zambia stands to benefit immensely, but with the right stake in the mining assets.

The question around whether the decision to restructure was done by the book is one that can not be overlooked because as highlighted earlier, the tug of war involving KCM is still undergoing arbitration yet resolutions were passed by for reorganization. Should the earlier assumption pass the goodness of fit test, then we can infer that the restructure decision was then overridden sovereignty where a nation reserves the right to take over or make decisions over assets in instances where it is proved that exploitation existed at the expense of citizenry.

Read also: Enough is enough, Zambia’s Head of State warns Vedanta and Glencore’s Local Unit

IT IS THE LAST STRAW THAT BREAKS THE CAMELS BACK

The initial license breaches cited in the commencement of liquidation proceedings by ZCCM-IH are highly likely what the provisional liquidator would lean on for justification of the recent developments in the best interests of the Zambian people. Additionally, the provisional liquidator according to the management brief, has support of the key unions such as the Mineworkers Union of Zambia (MUZ), National Union of Mining and Allied Workers (NUMAW) and the United Mineworkers Union of Zambia (UMUZ) reflecting the consensus of the employees.

Globally, Vedanta grappled with delisting from the London Stock Exchange (LSE) following pressures from various groups and litigation that began to erode its share price.

Read also: Zambia’s Environmental Management Agency takes a sulphur dioxide swipe at Vedanta’s subsidiary

ZAMBIA LOOKS TO THE MINING SECTOR TO CLAW BACK ERODED GROWTH

Africa’s copper producer will according to the Economic Recovery Plan (ERP) 2020 – 2023 seek to leverage of the mining sector to aid growth recovery. Speaking in his speech, Zambia head of state Dr. Edgar Lungu encouraged mining exploration to widen production capacity while hinting an increased stake holding in key mines.

“Owning a stake in some strategic mines gives the state the leverage required to utilise the defined mineral resources to benefit the nation,” President Edgar Lungu said during the launch of the Economic Recovery Plan (ERP).

“I must mention that this is not nationalization of the mines, on the contrary, it is the state acquiring majority stakes in selected mines while allowing private investors to also participate in the sector,” he added.

A RESTRUCTURE AS THE RED METAL HOTSPOT TALKS WITH THE IMF

Zambia has had its fair share of economic woes key of which includes an elevated debt stock position totaling $12.97billion for which it seeks a fully funded package from the IMF and has commenced a restructure process with the hiring of Lazard Freres. The recently launched economic recovery program addresses reforms in key sectors such as mining through review of tax regime to be achieved through an indaba in 1Q21. However it is not a secret that Zambia’s shareholding in the mining sector has been a major anomaly which has prompted the state to rethink this ownership as what is obtaining in the case of KCM.

It is also vivid that the state must acknowledge that it does not have the technical capacity to run mines but could best address the anomaly of shareholding structure by partnering with more experienced and competent equity partners that should invest in these entities to benefit the citizens and the country as a whole. Zambia remains closely watched by key partners such as the IMF and that execution of decisions could have implications. However what remains critical is which equity partner the authorities settle for especially in their track record and ethical standing in th best interests of the Zambian citizens.

Zambia remains spoilt for choice of equity partners with the likes of Anglo America who are back in Zambia, exploring for minerals and the Chinese with deeper pockets who have keen interests in Zambia’s mining assets.

The current mining quagmires may be a bittersweet experience for Zambia but the recent developments do send a stern signal to investors especially concerning exploitation of citizenry. However the execution of these decisions has potential to scare away investment and as such what should be sought is a balance for a win – win outcome. In conclusion one line describes the restructure and reorganization move is that sovereigns will always be sovereigns, investors should always seek to optimize benefits that are citizen centric.

The Kwacha Arbitrageur