A RATE DECISION MEETING WITH A FISCAL SKEW

The central bank in Africa’s second largest copper hub will have deliberations for its second rate decision meeting of the year 2019 next week on 21-22 May. Zambia currently grapples with a currency slide quagmire amidst falling foreign exchange reserves that have weighed investor confidence thereby exacerbating asset – sell off pressure in both the foreign exchange and money markets. Market players have for the last few seeks sought clues as to what Denny Kalyalya will announce at the peak of next week’s MPC meeting.

Read also: Anemic Kwacha debt sale outcomes persist as BOZ takes another haircut in bond offering

From last MPC, Zambia has had a fair share of bearish waves on yields both in the short and long term with government securities paying as high as 26.2501% in the 1 year as the 5 year bucket widened to 30.5% in the last respective debt sales. The money markets have taken 11 out of 12 haircut in subscription spelling deficits in government funding for its fiscal programs. Secondary market trading used for price discovery revealed that primary market yields have been for a while priced at spreads below the perceived sovereign risk of the Zambia. Correction was nonetheless appreciated in the last bond sale that saw liquidity spreads widen 500-550 bps pushing bond yields 29.5% – 30.5% between 2-5 year tenors as 9 month and 1 year paper jumped 175 – 220 bps. These moves corrected the persistent inversion in the Kwacha money demand curve. At some point in the year, the 1-year treasury bill was the most attractively yielding asset in the money markets. We analyze yield curves because credit pricing for facilities by commercial banks reference the government security curves more than the benchmark lending rate which only determines the credit spread provided by the difference. (Credit spread = Government security yield less monetary policy rate). Investment and corporate bankers will weigh the opportunity cost of booking deals to just locking up liquidity in bills and bonds.

Read also: Yields on 1-yr Kwacha treasuries jump 220bps

Read also: The odds of Bank of Zambia hiking rates in May MPC

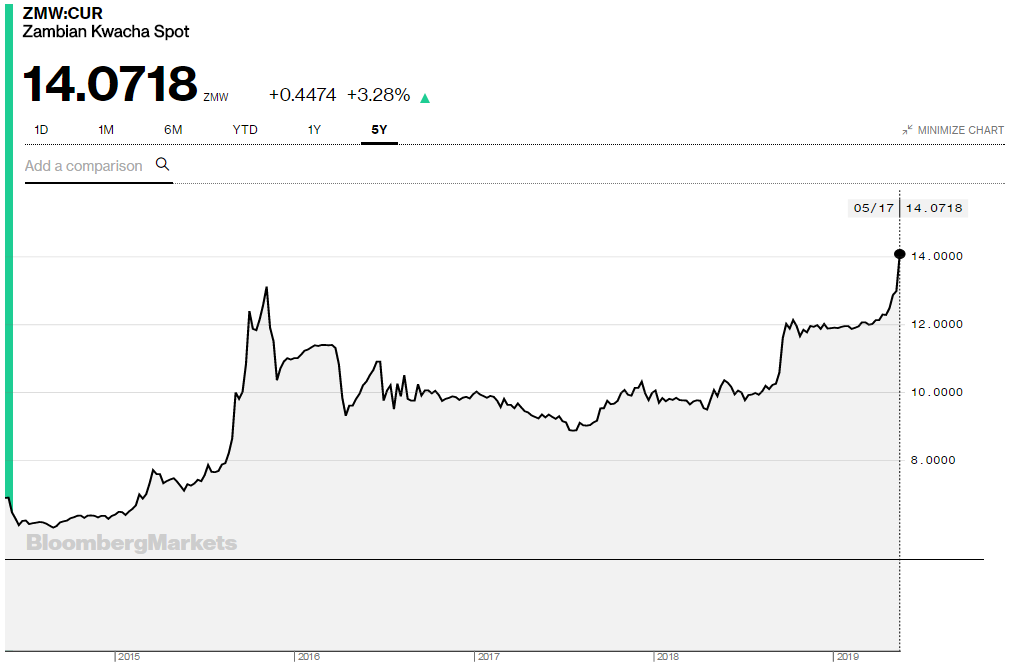

Sentiment has been the largest driver of financial market behavior fueled by falling reserves and persistent balance sheet vulnerabilities which multilaterals like the International Monetary Fund and World Bank have highlighted. Reserves are currently at 1.7 months of import cover at less than one and half billion dollars which has opened up the economy to vulnerabilities to stress shocks. With the Bank of Zambia out of the currency markets it has been very hard to tame the Kwacha that is on a weakening streak and is trading above 14 for a unit of dollar. Uncertainty has additionally fueled speculative dollar buying resulting in increased demand for the safe haven currency. In fact the dollar has been forecast to reign for 3 – 6m given the current global macro backdrop given trade impasse, geopolitical tensions and Brexit autopsies respectively. London Metal Exchange (LME) Copper on the other hand as a bell weather for economic prospects has been stagnant between $6,100 – $6,550 a metric ton though the deficit is expected to widen and thereby will provide support to rally the red metal to $7,000 a metric ton in H2.

IS THIS A DEJAVUS OF FOURTH QUARTER OF 2015?

Primae facie, it looks like a repeat of a cycle that Zambian markets have seen before save 2015 had lower debt service and higher reserves than the current state of affairs. Currency slide to 3.5 year lows was last seen in the week leading to the 19 Nov. in 2015 which triggered the Bank of Zambia to hike rates by 300 bps to 15.5% which was tagged by many analyst as a reactive rather than proactive response. The markets had from Oct15 been screaming rate hike when the Kwacha hit an intraday low of 14.2.

The other dejavus is the reactive nature rather than proactive stance of the central bank to act in turbulent times. We would have expected an emergency MPC meeting to tame the currency slide but this has not been the case with the Bank of Zambia that have stuck to their calendar.

The role of stabilising a currency lies with any central bank. Uncertainity due to lack of information can cause anxiety and panic buying. Could someone take leadership and assure the market?

Economics Association of Zambia President Dr. Habazooka carried on his social media page

Read also: Speculation drives Kwacha to 3.5 year lows

Will the BOZ adopt a similar approach on 22 May? With limited ammunition (reserves) to ease currency pressure and zero latitude for stimulus, all odds point to a rate hike. What we are not sure about is the quantum. History tells us that the widest jump every seen is 300 bps (3%). Liquidity may have to tighten through hiking the statutory reserve ratio and the benchmark may have to be pushed higher. The extent of the hike on both MPR and SRR will be determined by the sensitivity to private sector growth needs.

BOZ has once raised the SRR to 18.5% causing a liquidity crunch in the market that penalized private sector growth and this saw the economy slow down to lows of 3.22% in gross domestic product growth from celebrated levels of 6.7% in good years. We attach an 80% chance of a 300 bps rate hike on both MPR and SRR next week if the rate decision making committee will be concerned about stabilizing the currency depreciation. The latitude the BOZ has extends to 575 bps but we believe if they decided to take that route then we attach a two rate hikes possibility for Zambia this year would be eminent. It is important for this move to be applied now as currency depreciation is a bigger evil in markets that could result in cost push inflationary pressures from higher crude import costs which if not addressed earlier spirals into bigger rate hikes.

WHAT ABOUT PRIVATE SECTOR GROWTH?

Business confidence is at a 2.5 year low with the Purchasing Managers Index – PMI April headline print of 45.2 in the red. Zambia’s private sector pulse has for 8 -months in a row been below 50. (50 is the borderline between expansion and contraction). It is clear that all commentaries point to elevated manufacturing cost curves as a result of higher fuel prices, wage bills and lack of liquidity in the sector.

Read also: Zambia’s April business confidence at 2.5year low – PMI

Input costs are rising and so are selling prices evidencing breeding inflationary pressure. Given the two options on the table whether to save private sector growth or curb a currency slide, we are of the opinion that that the latter is a bigger evil and hence more urgent to address and as such we believe if the Monetary Policy Committee – MPC are experienced enough to move in with money market tools to arrest the depreciation.

HAS MONETARY POLICY BOTTOMED?

It is very evident that with a BPR of 9.75% given the current government security yields, inflation and the SRR level that monetary policy has bottomed. Suffice to say, there is very little latitude for stimulus using monetary policy tools. What is clear is that the fiscals have elevated and there is need to have them realign to the monetary side for equilibrium. If this does not happen there will always be something that has to give and this case interest and currency will continue elevating. Credit risks remain elevated and Zambia risks lower assessments with the rating agencies especially that Moody’s in a note warned that it could be thinking of lowering the current Caa1 (stable outlook).

We expect next week’s meeting to be a rate decision meeting with a fiscal skew. Markets have already given clues through a depreciating currency, elevated government security yields and widening credit default spreads on dollar bonds.

Compiled by The Business Telegraph Markets Editorial team

1 Comment

Pingback: Kwacha flirts with lows of 14 as Dollar demands ebbs higher | The Business Telegraph