As meat prices in Africa’s second largest copper hotspot, Zambia continue to scale higher for beef, chicken and fish the food component of the Consumer Price Index – CPI continues to weigh overall inflation. According to the Zambia Statistics Agency – ZSA report for June, annual inflation accelerated 140 points to a 19 year high of 24.6% fuelled by a 2.7% rally in food inflation to 31.2% while the non food side was unchanged at 17.1%. Monthly overall inflation decreased to 1.3% from 2.0% in May. Monthly food inflation decreased to 1.5% from 2.5% compared to monthly non-food inflation that eased 0.3% to 1.1%. However the decelerated month on month pace seems to suggest that annual inflation could be at its peak.

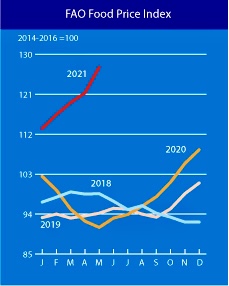

Zambia is experiencing effects of a global systematic quagmire given that food prices across the world have spiked 40.0% as measured by the Food Index, in the last 10 years according the Food Agriculture Organisation – FAO. See the table opposite. Global wheat prices remain elevated as demand in China soars pushing prices high which has continued to weigh feed prices across the board. Value chains remain constrained by an array of factors ranging from diseases such as Avian flue and foot and mouth disease etc. Drought effects continue to weigh value chains which has impacted the industry. Sixty to seventy percent (60.0-70.0%) of Zambia’s meat is supplied by small scale farmers who continue to bear the brunt of droughts and disease affecting poultry, cattle and piggery business. A global soya deficit is driving prices higher within a range of $520 – $550 per ton contributing to higher meat prices which is reflecting in the CPI. However bumper harvests and an improved precipitation posture could in mitigation offset some of the input pressures to ease feed prices in the medium term. On the positive, rising meat prices are motivating small scale farmers as margins are fairly healthy.

Read also: Beef and fish scale Zambia’s May inflation 150 points higher

Amidst a debt crisis and a deepening pandemic, inflation remains the biggest quagmire as the cost of living continues to soar at a time that the Southern African nation is 49 days to an August poll. These levels that inflation has flirted with are one the copper producer has not seen in over 16 years. The red metal producers inflation climb has been a function of cost push pressures whose roots still trace in a weak currency trajectory whose intensity was heightened in pandemic era. Asides currency depreciation induced price speculation, demand pull inflationary effects are evident in the stimulus package effect by the central bank in cushioning pandemic induced credit risks. Despite rising food inflation a bumper harvest as announced by the authorities is likely to moderate the rise in non meat related products such as maize meal.

GLOBAL INFLATIONARY PRESSURES ARE TRANSMITTING TO EMERGING MARKETS

Global inflationary effects are forecast to transmit to emerging markets as shipping and freight costs spike as COVID related disruptions constrain supply chains in addition to geopolitical tensions that are pushing crude prices higher. Inflation could transmit to dent manufacturing pulse as inout inflation remains elevated in the supply chains. Zambia’s May Purchasing Managers Index – PMI slid into contraction by 0.4 points to 49.7 after expanding for the first time in 26 months to 50.1 in April. Pandemic risk remains a major threat to the supply chains.

In addition to widening the cost of living, Zambia’s inflation spiral has sent the treasury bill curve deeper underwater 140 basis points as all tenors save the 1-year currently yield below 24.6%. However this is of little concern to offshore players who are more concerned about the exchange rate and the current inflation levels still below bond yields but has eroded risk premiums for those with appetite for government securities.

The Kwacha Arbitrageur