According a risk note by Fitch solutions, Zambia’s real GDP growth will slow to 3.0% in 2019, from an estimated 3.8% in 2018. This will be attributed to the proposed tax regime to be implemented from January 2019. Fitch solutions projects this will weigh on mining sector productivity despite the positive outlook for copper prices.

Challenging weather conditions will further weigh on agriculture in the short-term and rising inflationary pressures will pose severe headwinds to non-mining sector activity, weighing on headline GDP going forward.

Poor implementation of key infrastructure projects will weigh on the copper producer’s construction sector to slow down economic momentum in the medium to the long term.

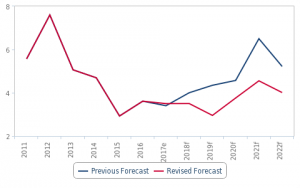

Zambia – GDP Growth, % y-o-y

Despite a positive environment for copper prices, the tax measures proposed by the government in the 2019 budget plan will slow activity in copper production, weighing on headline GDP growth over 2019.

Fitch has for a long been highlighting that Zambia’s worrying fiscal dynamics and structural obstacles to reducing the size of the government’s fiscal deficit increase risks to the business environment in the country. The research agency believes that tax increases in the mining sector – which include, amongst others, a 1.5% points increase in mineral royalty taxes across the different price bands and a reintroduction of sales tax in lieu of value added tax – will significantly increase business operating costs, pushing a number of mines into loss-making positions and discouraging further expansionary investments.

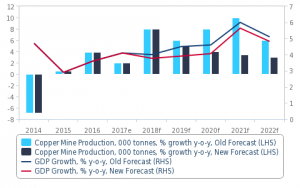

Downward revision on copper forecasts to 5% next year

Fitch has revised down its forecast for copper production growth in Zambia, to 5.0% in 2019 (from 6.0% previously) and 4.0% in 2020 (from 8.0%). As the mining sector accounted for 15.8% of total value added to GDP in 2017 – the second highest share in the economy after wholesale and retail trade – this is a slowdown in production that will weigh on headline economic activity, decreasing GDP growth to 3.0% in 2019 and 3.8% in 2020, down from an estimated 3.9% in 2018.

Zambia – Copper Production and GDP Growth, % y-o-y

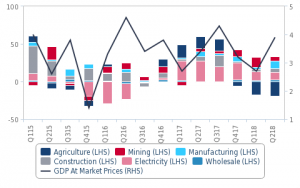

A slowdown in non-mining sector activity will also weigh on growth over 2019 and 2020. While headline GDP growth increased to 3.9% y-o-y in Q2:18 from 2.7% registered in Q1:18, activity in the agriculture sector experienced a 19.2% decline in growth in Q2:18, and Fitch expects growth will remain muted due to challenging weather conditions. Indeed, a drought between November 2017 and February 2018 hit production in the 2017-18 season, reducing maize production by 35.0% in 2018.

As the government’s fiscal challenges led to a reduction of farmers’ subsidies under the Farmer Input Support Programme in the 2019 Budget, Fitch believes planting during November will likely be below averages, weighing on the 2018/19 harvest.

Finally, further downside risks to production posed by the El Niño oscillation, whose recurrence is forecast with a 70.0% chance by the World Meteorological Organization (WMO) and which could lead to significant distress and droughts during season.

Zambia – GDP Growth by Sector, % y-o-y

At the same time, a recent appreciatory trend in the Zambian kwacha will lead to higher inflation, further limiting already vulnerable household and business consumption.

The kwacha lost 19.3% of its value against the dollar between January and November 2018, and it is believed that lack of confidence in Zambia’s debt markets will continue to put pressure on the unit. The resulting uptick in inflation, coupled with our expectations for more hawkish monetary policy by the Bank of Zambia, will constrain credit to households and businesses, weighing especially on the wholesale and retail trade sector, which accounted for the highest share of growth in the economy (19.0% in 2017).

Zambia – Incremental Capital Output Ratio (ICOR), Zambia, 2005-2017

Finally, poor project implementation coupled with limited fiscal resources will weigh on Zambia’s GDP growth over a longer time frame.

We expect real GDP to register lower growth rates over the next decade, averaging 4.2%, down from the 6.2% registered in the past decade. This will be mainly due to the poor implementation of many infrastructure projects. While promoting necessary investments into transport and energy infrastructure – which remain one of the major obstacles to Zambia’s sustainable long-term growth – the government has struggled to address structural issues related to how spending is allocated, delaying or failing to complete important projects such as the Link-Zambia 8000 road project. Indeed, Zambia’s incremental capital output ratio – a measure that assesses the marginal amount of investment capital necessary for an entity to generate the next unit of production – has increased dramatically since 2012.

Government’s structural fiscal challenges will persist, weighing on infrastructure and construction sectors in the medium-to-long term.

Source: BMI Fitch Solutions