The monetary policy committee in Africa’s red metal producer will on Wednesday 20 November announce its monetary policy stance for the next quarter at 10.30am. Amidst a deepening energy crisis the Finance Ministry is spending $27 million monthly to plug part of a power gap through a 300MW importation from South Africa’s Eskom given receding dam levels at the Kariba, Itezhi tezhi and Kafue stations. Business pulse has lost steam with headline Purchasing Managers Index below 50 for 14 straight months. Growth is suppressed with the years forecast at 2.2%.

Barely a week to the rate decision meeting the Bank of Zambia in an inflation reigning campaign, hiked the overnight bank rate by 1,000bps to 28% the highest the central bank has every charged since December 2015 when the OLF rate rose to 25.5%.

In the May MPC session Dr. Kalyalya hike rates by an infinitesimal 50bps to 10.25% which many Analysts believe was inadequate action given the risks to growth. Historically in 2015 December MPC, Kalyalya has hiked rates 300bps to a record 15.5% in a move to curb a sliding currency during the Kariba crisis where the copper producer grapples with energy poverty of 900MW.

Speaking during a MoneyFM behind the markets on Tuesday 19 November, Financial Analyst Mutisunge Zulu who also serves as National Secretary of the Economics Association of Zambia said fiscal inertia could this time force monetary policy tightening if the currency slide is to be tamed from current levels.

“We believe the central bank has latitude to hike not only rates but the reserve ratio to tame the Kwacha depreciation but it will be at the expense of private sector growth, a tough lesson learnt from the 2015/2016 energy crisis era,” he said. The fundamentals are feeble given the energy crisis and funding needs that are exacerbating dollar demand and at a time reserves are low, is causing one way traffic as the depreciation worsens which would cause the BOZ to tighten policy aggressively, he said.

The dislocation between the fiscal and monetary side is an issue the central bank has grown weary of in Africa’s copper producer as it grapples with rising debt, falling reserves and suppressed growth.

We attach an 80% likelihood of some form of monetary policy tightening in tomorrows announcement to be triggered by the need to tame the currency. Earlier we were convinced this MPC would have no change after the OLF communique but very minimal effect post the bank rate hike has been seen this far requiring more action. The central bank could exercise its latitude of up to 150bps of the 525bps to a historic 15.5% it has if it so wishes. But because the economy needs to breath and grow a smaller dosage is anticipated.

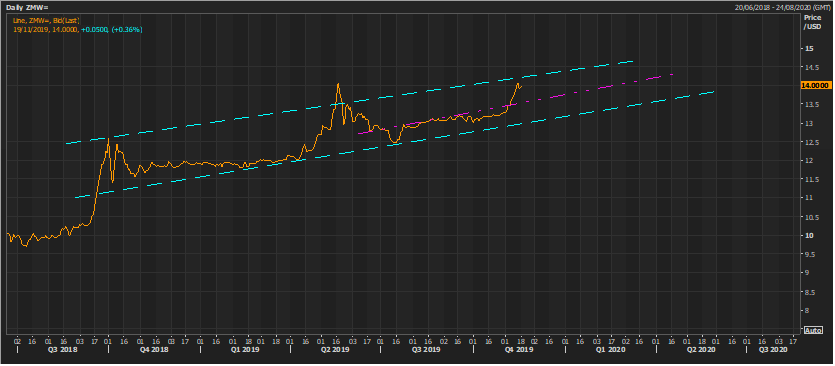

The Kwacha Arbitrageur