Emerging and Frontier Market (EFM) government securities continue to attract global liquidity as the inflation ghost in the west haunts thin treasury yields in a negative premium bubble. Offshores have flocked the government securities markets in Kenya, South Africa, Uganda and Zambia providing support to respective local currencies from dollar inflows. Zambia’s July 23 government bond auction was oversubscribed which 99.0% of liquidity housed in the 2,3 and 5 year tenors while the longer dated portion saw very anaemic appetite. This distribution skew reflects risk aversion by offshores about Zambia weighed by the current economic posture gyrating between rising metal prices and positive strides towards restoration of fiscal fitness on one end and the red metal producers default rating necessitated by non payment of dollar bond coupons. In our earlier analysis, it was explained that appetite for government securities is more an offshore hunt for yield given the state of the global economy than sentiment from developments relating to talks with the Washington based lender, the IMF.

HOW FRIDAYS BOND SALE OUTCOME SPELLS THE TERM ‘RISK AVERSION’

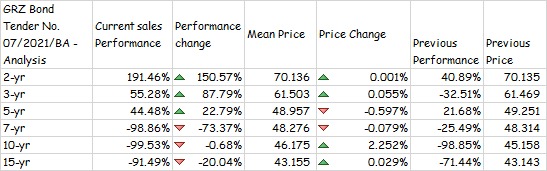

The highest interest was observed in the 2 year tenor whose sales were up 150.6% however with a close to zero price change compared to a 40.9% in the previous auction while appetite for 3 year bonds saw a 87.8% with a marginal price ebb as the 5 year performance was the least at 22.8% as price edged higher by 0.29. The 2 year zero price change highly signals potential rollover of investment maturities.

The Bank of Zambia sold K1.64 billion worth of 2,3 and 5 year government securities of the K1.5 billion of assets on offer with yields in the 3 and 5 year tenors climbed 100 basis points to 31.49% and 32.99% respectively. Sovereign risk posture continues to price into investor decisions as they exhibit duration preference in their vast portfolio mix. The S&P Zambia sovereign bond index continues to reveal real positive real dollar yields for investing in government securities in comparison to US treasuries whose premiums are negative.

For as long as debt restructure concerns exist, risk skew will persist towards shorter dated higher yielding assets except for in exceptional circumstances such as when local pension funds locking liquidity for liability management programs. Zambia is 3 weeks away from the August polls to elect national leadership for the next 5 years and as such political risk factors still links to the copper producers outlook post August 12 to implement the agreed macroeconomic framework with the IMF as the Southern African nation seeks to secure and Extended Credit Facility. Other mild confidence drivers include the IMF COVID relief funds in increased Special Drawing Rights – SDRs which will provide Zambia and every other nation additional funds to finance vaccines that will help contain the pandemic which is the biggest threat to growth currently.

The copper producers currency continue to take a cue from the dollar inflows from increased appetite, mineral royalties in the wake of all time high copper prices which has fuelled a 9.75% rally in the last 7 days straight which the Kwacha trading for a 9 month high.

The Kwacha Arbitrageur