The genesis of 2021 was characterised by healthcare response quagmires as the world was at varying levels of the COVID pandemic, safe to say the corona virus was still top risk surpassing climate change. Nearing the end of the previous year medicinal breakthroughs through vaccinations did rally markets as hope for economic recovery through rising demand pulse seeped through the world. Much as vaccines spelt hope, not all nations were ecstatic about this as it was still vague as to how developing nations would tap into accessing the worlds inoculation agenda let alone most nations Zambia inclusive pondered on threats of the second wave attack from stronger variants of the virus. For Africa’s second largest copper producer Zambia, 1Q21 was the most acute in case spikes through a strenuous variant of the COVID19 virus. Inferring from the 2020 experience, business ecosystem impact was forecast to worsen and this would add more fiscal burden following an earlier streak of dollar bond coupon defaults that dwindled sentiment sharply. In the labyrinth of a debt restructure, rising inflation and currency rout growth was projected to expand at an infinitesimal pace of 0.6% in 2021 (World Bank) and doubling to 1.2% (2022). Seconds before dawn, faster recovery in China, the Eurozone and US awakened a commodity rally that has seen base metals jump to levels not seen in decades.

Red metal prices continue to bellwether global recovery with a super strong come back from a trough of $4,343/MT to a peak of $10,740/MT on the London Metal Exchange – LME in the month of May. Prices have since eased to $9,989/MT following China’s stepping up the fight against rising commodity prices. Supply and demand factors continue to play a key role in fuelling the price climb. The biggest driver in fact has been global decarbonisation efforts towards cleaner energy and a multi trillion dollar US Biden infrastructure pronouncement, demand drivers, and supply disruptions through strikes in Chile.

COPPER BULLS JUST THREW ZAMBIA A LIFE LINE WHEN IT MATTERED THE MOST

For a nation like Zambia with an economic landscape shaped by a default rating status on its Long Term Issuer Risk on both local and foreign currency, spiralling inflation and constrained growth in the middle of an International Monetary Fund bail out package negotiations for an Extended Credit Facility – ECF, the copper rebound is a game changer for the Southern African nation. The mines remain the major foreign exchange suppliers to the Zambian dollar market for which higher red metal prices entail wider tax proceeds from the mining entities and a quicker shoring of foreign exchange reserves.

EMR Capital owned Lubambe Copper Mine operation in Chililabombwe on the Copperbelt Province of Zambia.

In the second rate decision meeting of the year, Bank of Zambia Governor Christopher Mvunga in his Monetary Policy Committee – MPC communique re-iterated that the central banks inflation forecast had changed for the better on the back of rising copper prices, a bumper crop harvest and improved sentiment inferred from a higher demand for government securities in the secondary market. These flows are tied to the ongoing BOZ bond buy back program as the central bank restructures domestic debt.

Bank of Zambia Governor – Christopher Mvunga speaks at the second MPC session of 2021 on May 19.

Higher copper prices help red metal exporting nations with absorption of dollar denominated obligations, build reserves and narrow fiscal deficits. Zambia’s reserves were reported at $1.2billion (March) in part a function of a weak export base as a consequence of low manufacturing capability and the countries net import position. Accumulation of foreign exchange has been low and as such has incapacitated the central bank from effectively intervening in the open market to price stabilise the exchange rate. It is for this reason that the Kwacha extended losses earlier effects of which where cost push inflationary in nature. Mvunga did assure the audience during his third MPC session that the reserve position had improved from March 30 levels which BOZ would yet announce in due course.

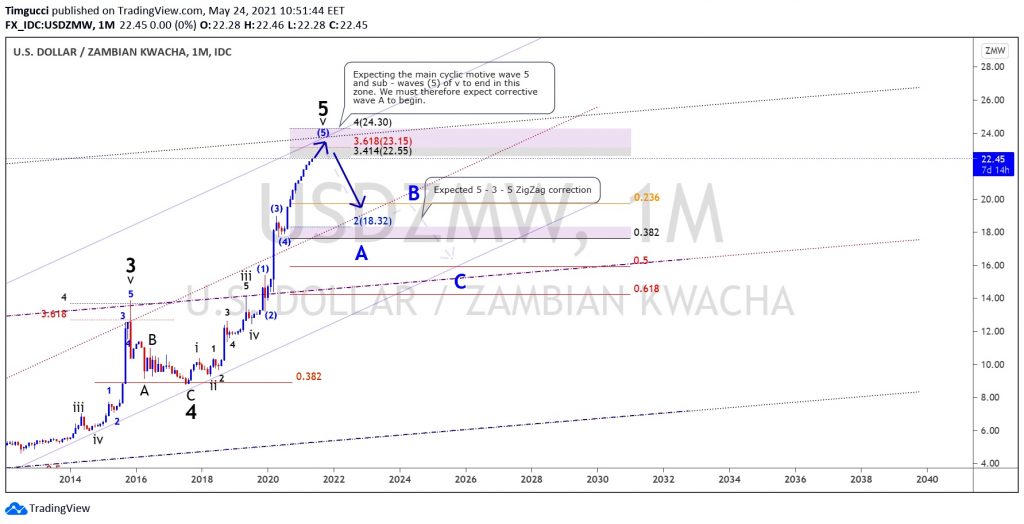

TECHNICAL ANALYSIS FORECAST OF THE KWACHA AGAINST THE DOLLAR IN THE SHADOW OF COPPER BULLS

The USDZMW price chart has two bullish ascending channels in which prices have been trending. Prices made an alternation around the 4th wave in July 2017 and created an extended impulsive wave 5. Currently, USDZMW is in its final advance of the extended motive wave 5 which should be expected to end at the vertex of its ascending resistance. The Fibonacci retracement levels around this zone lies around 3.618 to 4.0, representing a resistance zone between 23.15 – 24.30 Zambian Kwacha (ZMW) against the US Dollar (USD). Fifth wave extensions are followed by swift price retracements and their occurrence as in the case of USDZMW gives an advance warning of a dramatic reversal in price and this will lead to appreciation of the Zambian Kwacha. We should therefore expect a corrective waveform after completion of impulsive wave v of 5 to complete the eight 8th wave cycle.

PROGRESS ON IMF TALKS IS SUPPORTING SENTIMENT, COPPER PRICE RALLY EFFECTS ARE STRONGER

Zambia remains at the cusp of an IMF deal which over the last few weeks ignited hope for the copper producer with odds of an ECF before the polls widening. However with parliament dissolution on May 12 it is vivid that a bailout package will only be on the table post August but the positive remains that a macroeconomic framework has been agreed with the Zambian authorities who are yet to provide a position on the way forward.

L-R: Zambia’s Secretary to the Treasury Fredson Yamba, IMF Mission Chief for Zambia – Alex Segura – Ubiergo, Zambia’s Republican President Dr. Edgar Lungu, Director of the IMF’s African Department and Bank of Zambia Governor Christopher Mvunga at state house on December 7, 2020.

With or without an IMF deal soon, the recent commodity boom provide Zambia an economic rebound atmosphere that the Southern African nation will seek to maximise through dollar reserve accumulation and potentially a sovereign wealth fund architecture to hedge against external shocks. Balance of payment support will further ease the current mismatched foreign currency supply versus demand which will in turn address the ease of doing business. It is expected that dollar hoarding, for classes that sought safe haven in times of stress or uncertainty, will ease up as supply increases. This will further ease pressure on the exchange rate and should the base metal boom persist, stronger growth will ensue. Upside risks exist in the short to medium term from agriculture input demand linked to the Farmer Input Support Program – FISP.

The currency price is forecast to ease towards year end into next year should the scenarios explained play out.

The Kwacha Arbitrageur