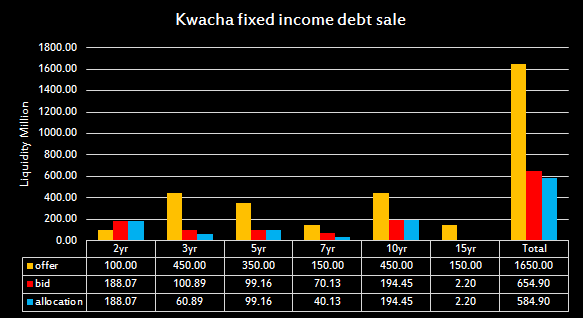

Central Bank in Africa’s copper producer, the Bank of Zambia, recorded yet another deeply udersubscribed Kwacha debt sale with K403 million (circa. USD$33 million) in assets sold on Friday 22 February. This compares to K350 million raised in December 2018’s debt sale and represents a 76% under subscription. Bid cover ratio was 0.24.

Despite K1,507 million of market liquidity as measured by aggregate interbank current account balance, bids totaled K655 million with the largest appetite in the 2 yr (28%) and 10 yr (30%) accounting for 58% of the total appetite. Of the total bids 62% were absorbed representing K403 million in allocations.

Read also: T-bill’s are suppressing appetite for bonds, the tale of an inverted kwacha curveL

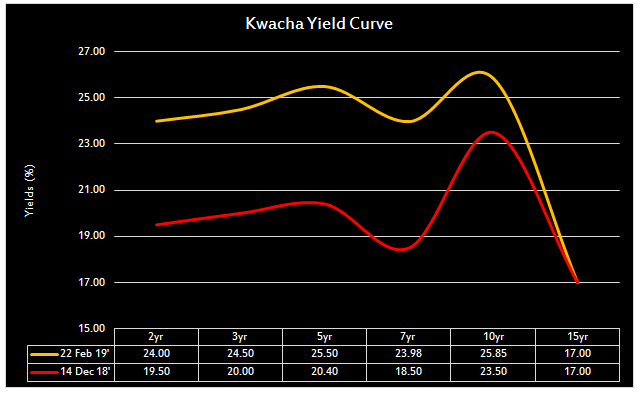

Kwacha bond curve corrects but t-bill pricing huge influence

The positive take away from last Fridays debt sale is the correction in term structure of Kwacha interest rates as a close reflection of the real credit risk profile of government assets. Suffice to say the fixed income assets were overstated the the quantum of credit spread correction. The yield curve widened by 235-548 basis points (bps) on the long end.

Read also: Widening spreads between ‘treasury-bill and swap’ yields could suggest overvalued Kwacha assets

The realization that bond yields were at credit risk spreads below what players perceived as market reflective sovereign risk for Zambia, drove the bidding interest rate behavior observed last Friday that resulted in elevation of the Kwacha curve higher. It was a week ago to last Friday more attractive to lock up liquidity in shorter dated higher yielding assets (treasury bills) than longer dated lower yielding assets (bonds). The primary market Kwacha bond curve was 300-350 bps below the 1-year treasury bill yields but after Friday 22 February the bond yield curve is between 48-235bps.

With increasing appetite for Kwacha assets offshore as global uncertainty looms, price discovery reveals that, players are now expected to shift focus across the entire Kwacha curve more balanced across treasury bills and bonds. This is likely to appreciated in the next bond offering 2- months ahead.

Rationality explanation for skewed appetite in 2 yr and 10 yr tenors

Friday’s government debt sale revealed stronger appetite for 2 yr and 10 yr paper. This was against the odds and the norm historically deviating from the 5 yr dubbed the sweetest point on the Kwacha yield curve. With the recent increased appetite for 1 yr bills, bids for 2 yr paper are explained by an expected risk averse – yet cautious approach towards locking yields. One would expect taking a gamble with a stochastic view of a 50/50 chance of an uptick and if they got it wrong, risk would fall off in 2 years. Two year bonds are a more cautious bet as they are closer to the 1 yr tenor. These are rational players whose decision to invest was shaped by the recent rising appetite for treasury bills versus the rising appetite for Kwacha bonds in the secondary market. The 10 yr government asset interest is surely from pension funds that ideally have appetite for longer dated assets to balance asset- liability portfolio mixes.