The year 2019 was a tough year for Africa’s red metal producer weighed by fiscal vulnerabilities and energy deficit woes. The need for climate change resilience can not be overemphasized with the need to market interventions to now be sensitive to weather pattern volatilities. The global ecosystem also had its fair share of instability with geopolitics, politics and trade wars impacting aggregate demand for key commodities like copper and crude oil.

This summary outlook outlines the 2020 forecast for Zambia with key driver explained below.

Geopolitical tension, political risks and trade war effects. Global risk themes into 2020 will remain geopolitical tension in the middle east driving crude price bulls, political uncertainty through Brexit, US impeachment quagmires and Hong Kong’s protests and the trade war impasse post phase one. These are the key themes that will drive commodity, currency and stock markets in 2020. Despite the uncertainty and volatility, 2019 remained the best year for stock futures given the steam build up running into the festivities when US halted additional tariffs on $156billion of Chinese goods and suspended tariffs on over $100billion worth of goods. The détente in risks to the end of the year has rekindled optimism around Chinese economic growth momentum to above 6% as the US remains the least dirtiest t-shirt in the global laundry basket.

Electricity and fuel costs. Elevated energy risks will suppress growth to below 1.5% for Zambia impacted by rising oil prices globally as OPEC+ member states increase supply curbs in March 2020 by 500,000bbls daily above the 1.2million bbl.. This coupled with Kwacha volatility skewed to bearish side will balloon oil import costs to spike inflation higher. Medium term forecast for 1H20 is between 14-16% given higher electricity tariffs and fuel prices. Inflation trajectory will be heavily dependent of central bank action to manage monetary policy.

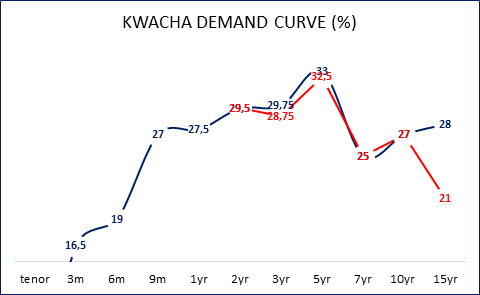

Fiscal spending to shape Kwacha yield curve. Interest rate risks remain elevated in 2020 for as long as government spending remains high. There is scope for government security yields to widen higher as evidenced by secondary market rates which reflect offshore perceived sovereign risks about Zambia. One year treasury bills closed 2019 at 27.5% while the 5 year bond yielded 33%. Treasury bills are still poised to outperform bonds in 2020 a reflection of risks appetite where players prefer shorter dated higher yielding assets as opposed to longer dated risker assets such as bonds. However an elevated yield curve as a benchmark for term debt pricing will cause an interest rate spiral to widen cost of funding to real sectors of the economy.

Low reserves and volatile Kwacha. Currency risks will persist in 2020 given the weak strategic reserve position at $1.4 billion. Interventions in place such as selling gold to the central bank are more longer term fixes than in the immediate term and as such the Kwacha will remain very vulnerable in 2020 with high likelihood of equilibrium shifting every time a record low is surpassed. However the central bank money market tools still have latitude to tame potential currency routs only at the expense of private sector pulse which will then suppress growth through higher funding costs and lack of liquidity through higher statutory reserve requirements. The Bank of Zambia has up to 15.5% on the benchmark interest rate, 18.5% on its cash reserve requirement inferred from historical 2015/2016 energy crisis era.

Weak business pulse. Private sector pulse is poised to remain anaemic, an extension of the three key themes from 2019 namely elevated operational cost environment, lack of liquidity and rising input inflation from currency volatility. Zambia has headlined PMIs below 50 for 10 months straight with one positive in 15 months. This weak pulse aligns with marginal growth expectations o blow 1.5%.

Resilient banking sector but smaller banks will struggle. Banking will remains fairly resilient at aggregate level from a capitalisation and profitability angle yet a few outliers such as the smaller banks are already bearing the brunt of higher funding costs and liquidity squeeze skews. Crowding out effects will benefit banks that will lock up excess liquidity through reinvestments or frequent rollovers in the government security market as they book interest income on banking books. Tough economic conditions will reverse the positive non-performing loan performance for 2019 of 9.4% (vs. 10% prudential limit). The NPL limit is forecast to be breached in 2020 given dampened credit appetite from potential downgrade risk and higher cost burdens on consumer to repay credit facilities.

Downgrade risks heighten as fiscal posture weighs. With risks to growth actualising from both the fiscal and energy sectors, it is highly likely that Zambia’s credit assessment will be lowered by Fitch/Moody’s/S&P to below CCC/Caa2/CCC+ which will cause a further blow out in credit default spreads on its 2022, 2024 and 2027.

Wider budget deficit than projected. Zambia’s fiscal deficit target of 5.5% could be a mirage and will have to be revised higher given the headwinds forecast from debt service, energy autopsy effects and weak domestic funding performance.

Unlikely IMF bailout package. A bailout package is very highly unlikely in 2020 given the elevated debt to gross domestic product in excess of 76% given the exchange rate risks which are a key driver of the computation. IMF bailout deal closure forecasts are more tangible post 2021 election given the perception around expenditure in years before and in the year of polls. However the Fiscal Head is more pro Brettonwood and will put the copper producer in good stead when the time comes. A good litmus test for fruitful engagement with IMF will be reinstatement of the resident representative in the Zambia office which the MinFin advised it was in talks with the Washington based lender.

Lackluster mining productivity. Mining globally will be supported by China’s growth momentum given the stimulus by Peoples Bank of China weighed by key developments such as Chiles productivity curbs given political unrest, Indonesia’s moving to different grades and Zambia’s power challenges and taxation environment. However Zambia’s mining landscape in 2020 will still be weighed by ongoing litigation involving top mines such as Konkola and First Quantum Mining (FQM). These developments could weigh productivity momentum. However Zambia remains a top coloured stone global contributor at its Gemfields Kagem and with a waiver of 15% export duty, emerald mining is poised to deliver better performance. Bullion mining in 21 districts with tighter security will spur mining growth and help build the nations strategic reserves.

The Kwacha Arbitrageur